Todd Vogt left empty-handed after browsing in the Louis Vuitton and Rolex stores in London’s upmarket West End shopping district this week.

The Canadian mining executive and his wife have made purchases before, but he said that their spending on luxury goods had “definitely” taken a knock as the post-pandemic economy remains sluggish.

“My wife likes bags from places like [Louis Vuitton] and I like watches,” he said, but added: “Prices have gone up . . . economic circumstances and the long-term economic outlook has meant that there are less luxury expenses in our household.”

The couple are not alone; the sense that shoppers have grown more cautious after a three year boom in global luxury spending is echoed by sales staff.

“We had a very good start to the year, but things have definitely slowed. There are less customers in the store,” one Louis Vuitton shop assistant said.

Over the course of the pandemic, the luxury industry grew at a record pace after shoppers stuck at home during lockdowns indulged themselves, boosting the longer-term trend of China’s growing affluent class scooping up monogrammed handbags and Dom Pérignon champagne.

Now, there are clear signals that a long-expected return to more moderate growth is crystallising as shoppers around the world rein in luxury spending.

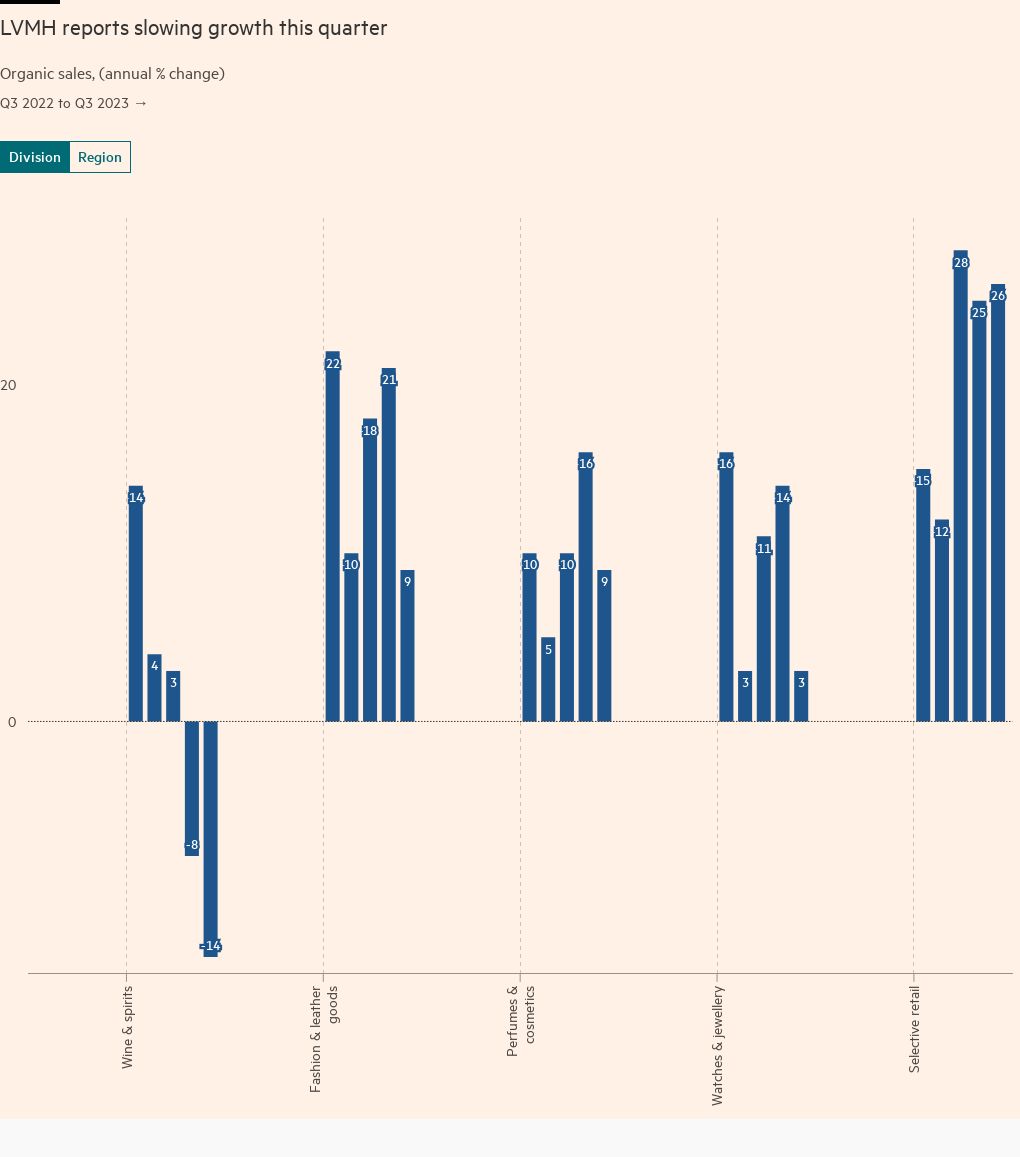

The impact was shown this week when industry leader LVMH, which is controlled by French billionaire Bernard Arnault, reported sales growth of 9 per cent for the most recent quarter, below consensus expectations and a steep slowdown from the 17 per cent increase it had recorded for the previous quarter.

“After three roaring and outstanding years, we’re converging toward numbers that are more in line with historical average,” said LVMH chief financial officer Jean-Jacques Guiony.

“Will we stay there? I don’t really know. There is no reason to believe that we will crash [or] that we’ll come back to the type of 20 per cent growth that we enjoyed for a certain period of time.”

Signs that the US was slowing down have been evident since the start of the year, but European markets are now also moderating as is growth in Asia — with the exception of Japan, where sales rose 30 per cent on an organic basis, partly as the result of an influx of Chinese tourists.

Sales growth in the US, the luxury industry’s largest market, edged up 2 per cent in the third quarter after flatlining in the second as so-called aspirational customers cut back on indulgences such as cognac. Europe is following suit, with revenue growth slowing to 7 per cent compared with 19 per cent as buyers tighten their belts.

The change of pace at the French luxury leader marked “an end to the roaring 20s”, analysts at Berenberg wrote as they cut back their outlook for the year. “This exceptional momentum was never going to last for ever . . . and the key debate now is what a ‘new normal’ looks like for 2024 and beyond.”

Led by big listed groups such as LVMH and Hermès, luxury has grown by an average of more than 20 per cent per year since 2020, according to consultancy Bain, whereas the industry’s historical average has been closer to 6 per cent.

An optimistic scenario this year would be 8 to 10 per cent, or 5 per cent in a more pessimistic case, according to Joëlle de Montgolfier, executive vice-president for retail and luxury at Bain.

“Basically, compared to last year, we are halving the growth rate in these scenarios,” she said. “It’s been extraordinary, but it’s absolutely not sustainable in the long term.”

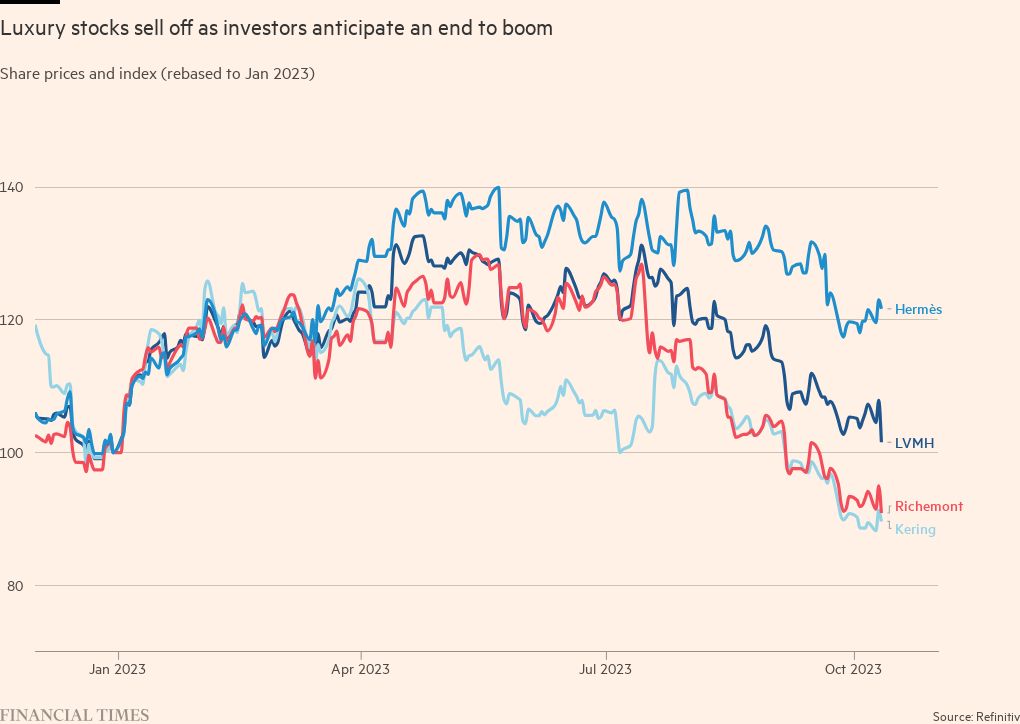

LVMH, which owns some 75 brands including Dior and Tiffany, is the first of the big luxury groups to report third-quarter sales, with peers Richemont, Kering and Hermès to follow in the coming weeks. However the French group’s size and influence means it sets the tone for the industry.

Luxury stocks have sold off in recent months from record highs as investors worried about the outlook for the sector; the Stoxx Europe Luxury 10 index has lost almost a fifth since its April peak. LVMH fell as much as 7 per cent on Wednesday, pulling down peers.

Customers are expected to pull back across all categories as the industry’s growth slows, according to Jean Danjou, luxury analyst at Oddo.

But he added that “hard luxury — jewellery and watches — is not growing as fast as soft luxury” categories, which include clothes, beauty and handbags, noting that jewellery sales tended to be especially exposed to China where there was increasing uncertainty about the direction of the economy.

At LVMH, wines and spirits — a category more accessible to aspirational buyers given its lower price point — was particularly hard hit. Sales fell 14 per cent on an organic basis in the third quarter, hit by softer champagne sales and a fall in demand for cognac, particularly in the US.

Buyers at department stores are also seeing changing shopping patterns and are adapting their inventories in order to cater to the more restrained mood.

“Designer businesses are in the toilet. Anything that was reliant on logo is not selling,” said a buyer at a top North American luxury department store. “I have some brands that are trading down 50-60 per cent compared to last year. I’ve completely divested out of designer [brands].” They added that they had reallocated their budgets to brands at more aspirational luxury price points such as Theory, Veronica Beard and Ulla Johnson.

Handbags continued to sell but customers were focusing on more accessible labels and hit bags from LVMH’s Loewe, the person said. Classic designers including Oscar de la Renta and “quiet luxury” labels such as The Row were still doing well, but “carrying some of those big LVMH brands, a lot of them are tough. The only thing that’s really weathering the storm in that sphere of very recognisable brands is Chanel and Hermès”, they added.

The more subdued mood reflects the tougher global economic outlook. While top luxury clients are more insulated from economic pressures such as inflation, the aspirational buyers — many of them young — who flocked to luxury brands in recent years feel them more keenly.

In Europe and the US, consumer spending power has been hit by inflation rising faster than wages. Researchers at Italian bank UniCredit found recently that rising prices had “completely eroded” the extra savings buffer that European households had amassed during pandemic lockdowns.

Retail spending in the EU was down 2 per cent in the second quarter from a year earlier, after adjusting for inflation, and the outlook is gloomy for the rest of this year.

“Eurozone consumer spending will continue to feel the pinch from the inflationary shock of last year with real household incomes hovering only just above levels seen at the height of the bloc’s sovereign debt crisis,” said Rory Fennessy, an economist at consultants Oxford Economics.

Ultimately a confluence of factors are pushing the luxury industry in the direction of moderation.

“Maybe people are starting to get bored of buying so many luxury goods,” said Danjou. “And then there is this macro pressure. With the combination of the two, you have a normal deceleration. But when a deceleration starts you never quite know where it will end up.”

This post was originally published on this site be sure to check out more of their content.